It makes sure statements like the cash flow are accurate and truly represents the company’s financial health. A post-closing trial balance is a financial report prepared at the end of an accounting period to ensure that all temporary accounts have been closed and the company’s books are balanced. Posting accounts to the post closing trial balance follows the exact same procedures as preparing the other trial balances.

Distinguishing Between Temporary and Permanent Accounts

First, the trial balance was incorrectly prepared and didn’t accurately transfer closing entries to the ledger account. Second, there may be a mistake while creating closing journal entries. Completing the accounting cycle correctly is crucial for corporate governance and truthful financial statements. It comes after closing entries are put into the general ledger.

How to Prepare a Post Closing Trial Balance

There may not be enough money to maintain this specialist in your enterprise if you have small start-up capital. For this reason, accounting services are becoming more and more popular. The Outsourcing companies offer their professional services for a relatively low price, so this offer is suitable for representatives of both large and small businesses.

Related AccountingTools Courses

The post-closing trial balance is a crucial component of the accounting cycle, serving as the final step before a new accounting period begins. It is prepared after all closing entries have been made and posted to the ledger accounts. This trial balance ensures that all temporary accounts have been closed properly and that only permanent accounts remain with balances.

AccountingTools

- However, most businesses can streamline this cycle and skip tedious steps like posting transactions to the general ledger and creating a trial balance.

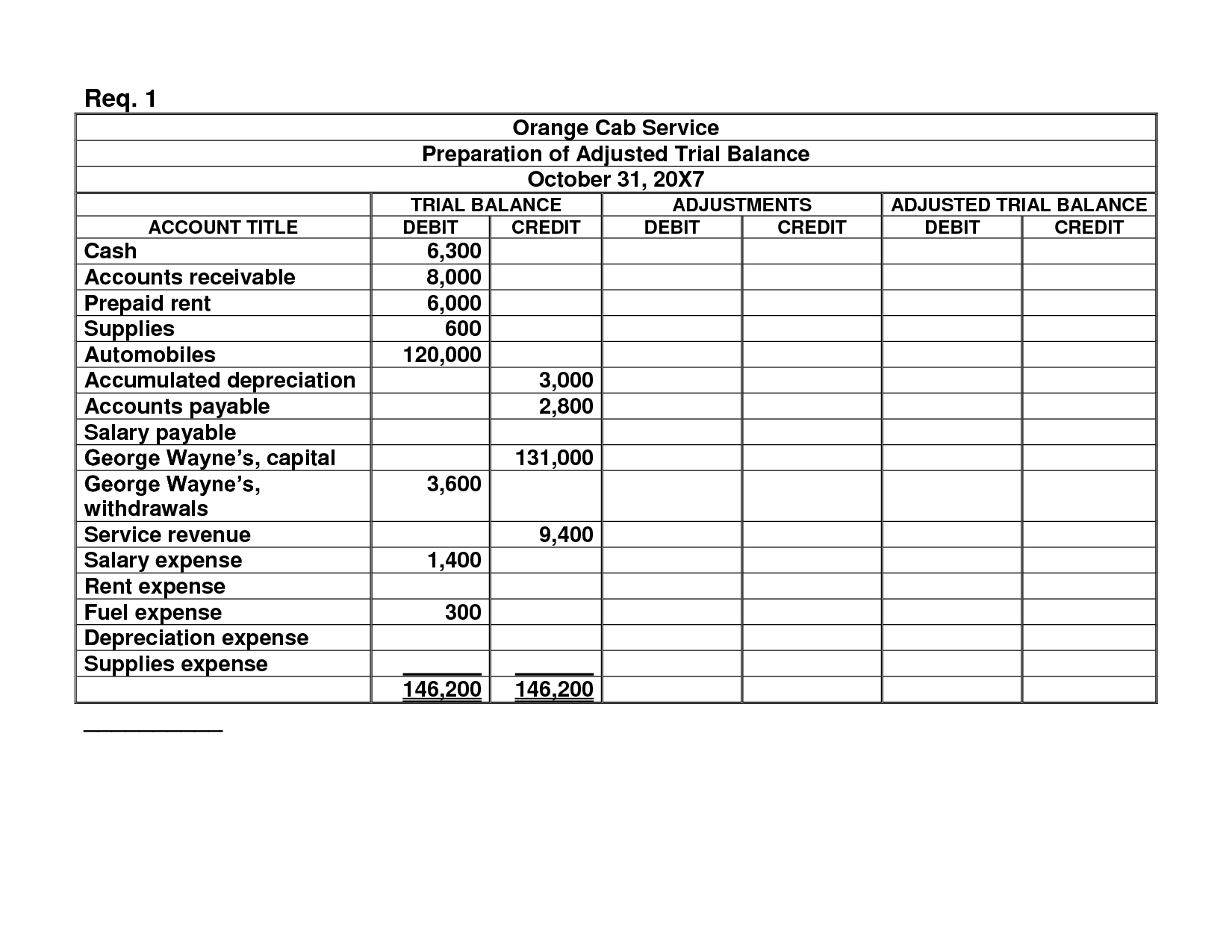

- Compiling a post closing trial balance is essentially the same as for unadjusted and adjusted trial balances.

- This step avoids simple mistakes and supports clear financial reports.

- Its key aspect is that it’s done after the period is closed, hence the name.

But, a post-closing trial balance only shows permanent account balances. For instance, accounts payable and cash stay the same between the pre-closing and post-closing trial balances. This highlights the role of these trial balances in keeping accounts clear. By following these steps, you can ensure that your post-closing trial balance is accurate and complete, providing a solid foundation for the next accounting period.

What adjustments are made when preparing a Post-Closing Trial Balance?

This is key for accurate accounting and reliable financial reports. Closing entries are essential for getting the general ledger ready for the new accounting period. This resets revenue, expense, and owner’s drawing accounts to zero. It affects important financial measures like the earnings retention ratio.

The post-closing trial balance is the ninth (and last) step of the accounting cycle. It can be prepared before the new accounting period begins and helps to prepare your general ledger for the new accounting period. The primary purpose of the post-closing trial balance is to ensure equality between the debit and credit to result in a net of zero. In addition, to ensure no more temporary or nominal accounts(revenue, expenses, withdrawal) exist before the books forward to the next year.

Trial balances of all sorts are done as a security measure. Without it, you can’t really be sure that your credited and debited accounts add up correctly. In short, while compiling the Trial balance, accountants check if all the deals done over this period are closed, so your paperwork is accurate and up-to-date. The what are temporary accounts fanda glossary above write-up provides complete information about preparing a post-closing trial balance. Apart from that, you will get detailed information about different types of trial balances. The total balances of the total debit and credit should be equal for continuing the new accounting period with zero net balance.

Thus, the post-closing trial balance shows the company’s financial health accurately. Similar to the financial reports, trial balances are prepared with three headings, which list the company name, type of trial balance, and ending date of the reporting period. Unadjusted trial balance – This is prepared after journalizing transactions and posting them to the ledger. Its purpose is to test the equality between debits and credits after the recording phase. The purpose is to check debit and credit equality after recording and posting closing entries. In conclusion, a post-closing trial balance is an important financial report for a company to ensure that all temporary accounts have been closed and the books are balanced.